Market gears up for policy meetings as Fed changes narrative

7 December 2021

Should he stay or should he go: Market impact if Boris Johnson holds on or resigns as Prime Minister

18 January 2022INSIGHT • 14 December 2021

The Convexity of Omicron

Kambiz Kazemi, Chief Investment Officer

“No one should be in any doubt: there is a tidal wave of Omicron coming” UK Prime Minister Boris Johnson, Dec 12th, 2021

“At some point next year, Covid-19 will become an endemic disease in most places.” Bill Gates, Dec 7th, 2021

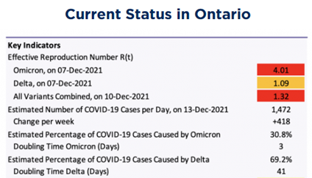

These two assertions fully characterize the uncertainty we are facing at this juncture with regard to the new Omicron variant. By now, experts agree that Omicron will overtake preceding variants (Delta and Alpha) with available data points presenting us with a staggering rate of transmissibility (R0) compared to previous strains. In Ontario, it has been transmitting at over 3x the rate of the Delta variant and is predicted to be the predominant strain by the end of this week, replacing Delta by Christmas!

Source: Ontario Science Table – Covid19 Advisory Board

At the time of writing, scientists are still looking to get a better grasp of omicron’s risks and its potential ramifications, but recent studies have found that Covid-19 vaccines may only be partially effective in fighting the Omicron variant despite its apparent lower severity. Still, the strain on the healthcare system could still be noticeable which might explain the haste and dynamism of some governments in reinstating some controls and restrictive measures.

As the precautionary principle goes, when it comes to pandemics, cybersecurity, geopolitical or investment risks alike: “plan for the worst and hope for the best”.

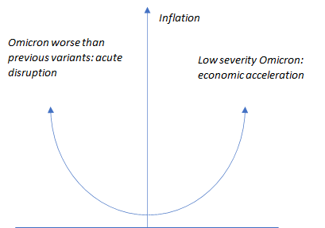

Omicron and inflation

At this stage the lack of visibility is a major impediment in trying to predict – even with a low level of accuracy – what the probability of various scenarios for different assets and investments might be.

However, this is where it gets interesting.

Whether Omicron turns out to be a milder variant and a potential turning point in this pandemic by rendering less acute and dangerous, or whether upcoming data proves it to be similar or worse than previous strains, there is a very high probability that Omicron will further fuel inflationary forces in either scenario. This is referred to as convex outcome for inflation: a good or a bad Omicron will drive it higher.

The good scenario: Omicron and the end of the pandemic in 2022

If Omicron’s turns out to have low severity and thanks to it transmissibility somehow ends up helping Bill Gate’s optimistic view materialize (Covid-19 becoming an endemic disease to humanity in 2022), then the euphoria we could witness will likely outpace that of last summer by many folds.

Some of the reasons for the ensuing rise in inflation, as mentioned on an earlier note ‘Inflation: Gone but not forgotten‘, would likely be in:

- A release of pent-up demand, further fueled by consumer’s ability to spend due to stellar return on their investments (both equity and crypto in 2021) and increases in wages.

- A synchronous pick-up in economic activity across the globe as the pandemic fades.

These factors will drive prices higher especially at a time when supply chains have not yet been fully reestablished and healed.

The negative scenario: Omicron is a worse variant all around

In this scenario, there are particular challenges with regard to:

- Supply chain disruption

- General mobility, cross-border freight and travel disruption.

These factors will likely be much more accentuated compared to the past episodes of the pandemic. A more virulent variant and higher transmissibility will have tremendous disrupting effect on labour intensive parts of the manufacturing industry, such as mining, construction or the food industry causing further imbalances both globally and locally in economies and resulting in higher prices. We will not expand here on many other challenges that this scenario poses and none of which is growth friendly, in fact rather the contrary.

Conclusion

Despite an uncertain path ahead due to the new variant, we assign a high probability to Omicron sustaining the existing inflationary pressures or even further exacerbating them.

And it is never too late to get ready, whether is by adjusting and tilting portfolios or by using appropriate hedging strategies and instruments.

Be the first to know

Subscribe to our newsletter to receive exclusive Validus Insights and industry updates.