Launching Open-Ended Funds: What GPs Need to Know

25 March 2026

Supply Shock: The Price of Infrastructure Destruction

7 April 2026RISK INSIGHTS

How Geopolitical Risks Are Splitting Central Bank Policy

By Validus | 26 March 2026 | 5 min read

Harun Thilak, Head of Global Capital Markets NA

The world’s major central banks held their latest interest rate decision meetings last week against a backdrop of escalating conflict in the Middle East, surging energy prices and heightened inflation risks.

The US Federal Reserve, Bank of Canada, Bank of Japan and Bank of England all opted to maintain policy rates unchanged. Yet, beneath the surface of steady rates lay markedly different forward guidance, with hawkish undertones dominating outside the US.

This divergence is now being priced into markets for the remainder of 2026, with the Federal Reserve telegraphing modest easing while peers signal tightening. The resulting policy split may have profound implications for global foreign exchange (FX) markets, tilting the balance toward non-USD currencies.

Key takeaways:

- Several of the world’s major central banks voted to hold interest rates last week, amid ongoing conflict in the Middle East and the resulting impact on the wider economy.

- While initial reactions seem aligned, forward guidance is split, characterized by marginal US dovishness versus tightening or accelerated normalization elsewhere.

- Investors should continue to monitor these developments closely, as these factors will dictate whether the current rate-path divergence will continue and, in turn, implications for FX markets.

How Did Central Banks React?

US Federal Reserve: Steady Policy with One Modest Cut in Sight

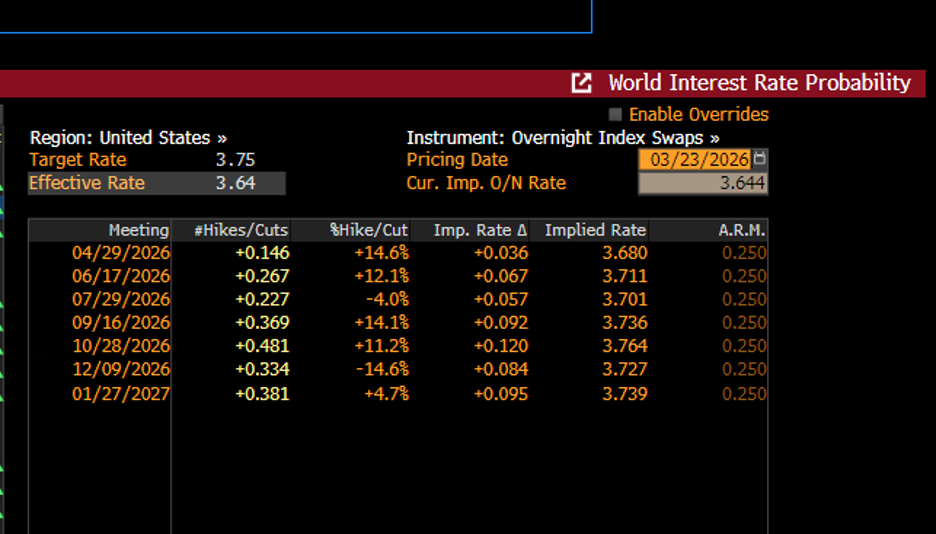

As widely anticipated, the FOMC held the federal funds rate target range at 3.50%-3.75% in an 11-1 vote on March 18. Federal Reserve Chair Jerome Powell acknowledged the risks presented by both energy prices and tariffs but emphasized that it remains “too soon” to assess the full impact.

The updated Summary of Economic Projections and dot plot reinforced a cautious easing bias; the median projection for the federal funds rate at end-2026 now stands at 3.4%, implying a single 25bps cut. Taking a closer look at the committee, however, seven officials see no cuts at all this year, while another seven anticipate precisely one.

Bank of Canada: Hold at 2.25% with Readiness to Hike

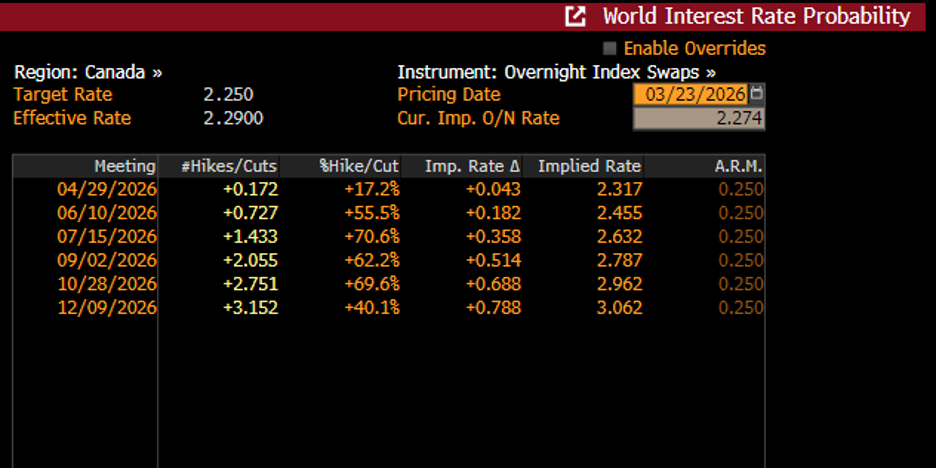

The Bank of Canada (BoC) kept its overnight rate at 2.25% on March 18, holding rates for a third consecutive time. BoC Governor Tiff Macklem’s statement highlighted downside growth risks from weaker activity and trade uncertainty, while flagging upside inflation risks from higher energy prices and potential US tariffs. The Governing Council explicitly stated that it “stands ready to respond as needed,” including hiking to prevent persistent inflation.

Bank of Japan: Unchanged at 0.75% but Normalization Remains on Track

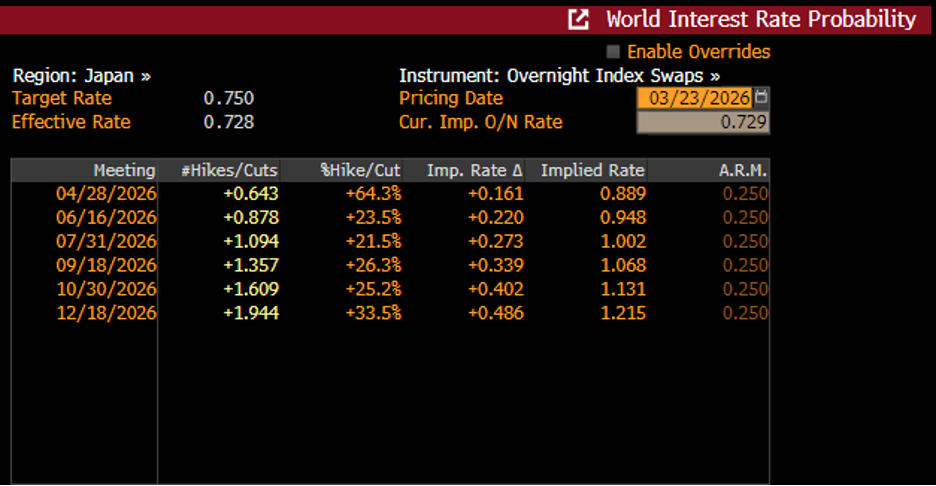

The Bank of Japan (BOJ) left its short-term policy rate at 0.75% on March 19 in an 8-1 vote, with hawkish member Hajime Takata dissenting in favor of an immediate rise to 1.0%. BOJ Governor Kazuo Ueda reiterated that the central bank will “continue to raise the policy interest rate” if the outlook for activity and prices materializes. He explicitly noted that real rates remain “significantly low.” The BOJ’s commitment to normalization—unchanged from January—contrasts sharply with the Fed’s easing tilt and underscores Japan’s determination to exit ultra-loose policy.

Bank of England: Unanimous Hold at 3.75% Turns Hawkish

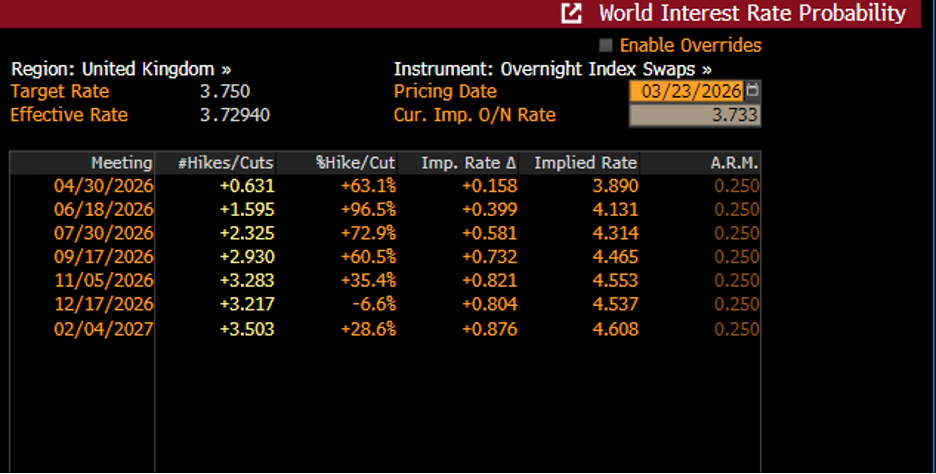

On March 19, the Monetary Policy Committee (MPC) voted unanimously to hold interest rates at 3.75%, marking a notable shift from February’s razor-thin split. Minutes from the meeting and BoE Governor Andrew Bailey’s remarks highlighted the upside risks to UK inflation from energy costs. The tone was also materially firmer than anticipated, with all dovish members from February’s vote aligning behind the hold.

Outlook for 2026: Clear Divergence Emerges

Following these meetings, the resulting repricing in Overnight Index Swaps (OIS) reveals a clear policy rate divergence amongst major economies. With the Federal Reserve’s median dot plot implying a single 25bps cut in 2026, US OIS pricing currently shows that market participants are anticipating US policy rates to remain broadly around the current levels for the remainder of 2026.

In contrast, the Canadian and UK OIS markets are currently implying almost three full 25bps rate hikes for the remainder of 2026 – up sharply from pre-meeting levels. Japanese OIS pricing, meanwhile, shows investors forecasting about 50bps of rate hikes for remainder of 2026, broadly in line with expectations pre-meeting.

This central bank policy divergence, characterized by marginal US dovishness versus tightening or accelerated normalization elsewhere, could become a dominant theme impacting FX markets as we head into the summer of 2026. In turn, potential USD weakness is expected in lieu of currency strength from the other G10 currencies.

Investors should continue to monitor energy prices, inflation prints, and other geopolitical developments closely as these factors will dictate whether the current rate-path divergence between the US and its peers widens or narrows, thereby driving the path for FX. For now, the message is clear. In a world of renewed inflation risks, central bank policy divergence is back, and the USD could start feeling the strain.

Chart 1: US policy rate trajectory implied from OIS markets

Source: Bloomberg

Chart 2: Canadian policy rate trajectory implied from OIS markets

Source: Bloomberg

Chart 3: UK policy rate trajectory implied from OIS markets

Source: Bloomberg

Chart 4: Japan policy rate trajectory implied from OIS markets

Source: Bloomberg