What GPs Need to Know: Managing Open-Ended Funds

9 April 2026

Ep 5: Hedging in Practice: What the Data Is Telling Us

19 April 2026RISK INSIGHTS

Peace talks fail: Risk considerations and market disappointment

By Validus | 15 April 2026 | 5 min read

Marc Cogliatti, Head of Market Risk Strategies

Key takeaways:

- Despite the ongoing conflict in Iran, markets rallied on hopes of a ceasefire, with oil prices dropping and both the S&P 500 and FTSE 100 nearing their all-time highs. However, this optimism appears fragile with no clear end for the conflict in sight as Iran’s nuclear ambitions remain a sticking point in peace talks, and the US imposes a blockade on the Strait of Hormuz.

- The risk on / risk off relationship between the dollar and equity markets is once again a key feature of the currency markets. Meanwhile, interest rates remain volatile as fears of persistent inflation have prompted markets to price out rate cuts from the world’s major central banks.

- Amid ongoing volatility, risk managers must prioritize evaluating hedging exposures, costs and liquidity risks.

Six weeks on from the first attacks on Iran and there’s little prospect of an imminent end to the conflict. While both sides have expressed their desire to end the war, Iran’s nuclear ambitions remain a sticking point following the latest round of peace talks. In response, the US has imposed a blockade on the Strait of Hormuz and pledged that the US military will “finish up the little that is left of Iran.”

Last week’s ceasefire helped restore an element of optimism to markets, triggering a ~20% drop in oil prices, a ~30bps drop in 2-year treasury yields and a ~4% rally in equities. As a result, both the S&P 500 and the FTSE 100 are marginally off their all-time highs. This is somewhat precarious, however, given that oil prices remain more than 50% higher than where they were prior to the conflict and the market has shifted from pricing in multiple rate cuts to multiple rate hikes from most central banks. Clearly there are other factors to consider beyond the Middle East conflict, but there’s a risk that the market is set up for disappointment.

What does disappointment look like?

Focusing on FX and interest rate risks, the risk on / risk off relationship between the dollar and equity markets is once again a key feature of the currency markets. This correlation is not as well defined as it has been historically, but the dollar has broadly benefited when equity markets have been under pressure and weakened when stocks have rallied. Sterling is once again showing its high beta tendencies, outperforming the euro when risk assets rally, but struggling when equities are on the back foot.

Meanwhile, interest rates remain volatile as fears of persistent inflation have prompted markets to price out rate cuts from the world’s major central banks. Instead, several rate hikes are now expected, with the Bank of England (BoE) notably predicted to raise rates by ~50bps before year end. Higher rates mean higher borrowing costs but also higher returns for our clients in the credit space.

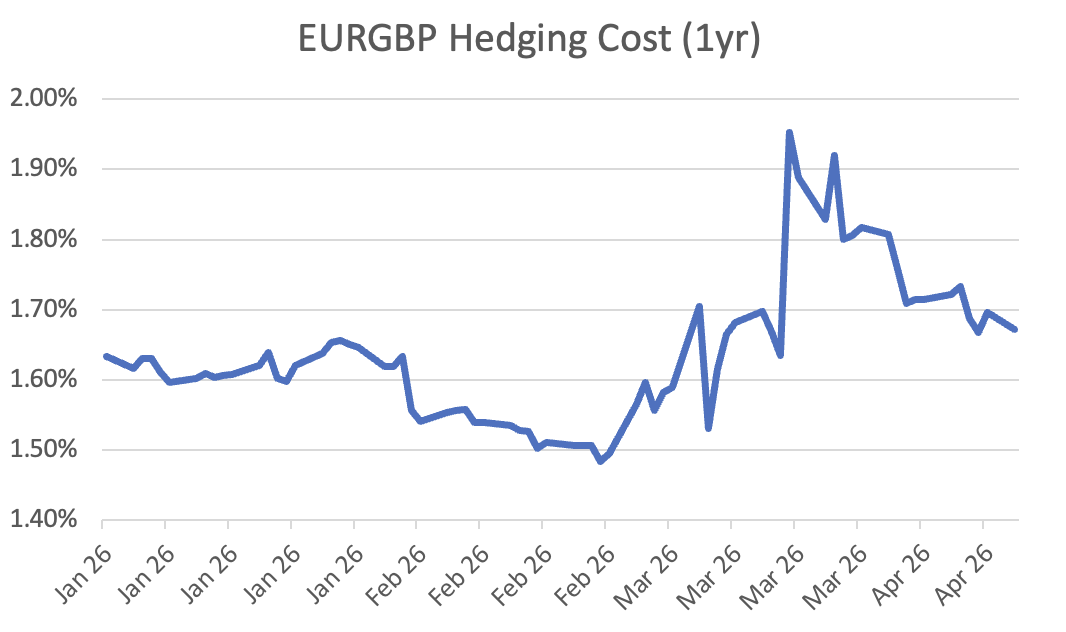

Interest rate volatility will also impact FX hedging costs as differentials widen (or narrow). For example, a European credit fund hedging sterling assets saw its cost of hedging rise from 148bps (excluding credit charges) to 192bps in a less than a month (see chart below) as the market shifted to price in three rate hikes from the BoE’s Monetary Policy Committee (MPC), compared to a more modest adjustment from the ECB. That has since fallen back to 167bps as expectations for the MPC have been pared back to two hikes.

Chart 1: EURGBP Hedging Cost (1yr)

Source: Bloomberg

The Validus Perspective

Aside from gazing into a crystal ball to predict market direction, three types of risk demand risk managers’ immediate attention:

- Hedged vs Unhedged Risk – When markets are particularly volatile and constantly in the headlines in the mainstream press, risk management becomes hot topic. Determining an appropriate hedge ratio is a challenge, not least because quantifying underlying exposures is often problematic. Too little hedging exposes the fund to undue levels of risk, but being over hedged can be just as problematic (if not more). Our Risk Advisory team is working closely with each fund / manager to determine the optimal solution for each of them.

- Managing Hedging Costs – Hedging costs arising from volatility in rates markets and the subsequent impact on interest rate differentials is proving challenging for managers. Blindly following a longstanding strategy without considering the impact of changing market conditions can be problematic and often result in an opportunity cost. However, frictional costs (predominantly spreads and credit charges) also warrant close monitoring as there’s a clear risk (and justification) of these rising during times of heightened volatility. This is being closely monitored by our Global Capital Markets (GCM) team who are working hard to ensure these costs remain stable.

- Liquidity Risks – Liquidity risks are often overlooked until they become an issue. Yet when they arise, they can be some of the most problematic for managers to deal with. Volatility can quickly result in large negative valuations for a hedging program, resulting in clients hitting CSA thresholds or credit limits with counterparties. Meanwhile, it isn’t untoward to see counterparties’ appetite to extend credit or take on additional risk start to dwindle during times of market stress. Fortunately, this isn’t something we’re seeing much of yet, but our ISDA Advisory and GCM teams continue to monitor this closely via our technology platform and counterparty relationships.