The Unstable (Hormuz) Ceasefire

6 May 2026RISK INSIGHTS

UK local election results and the impact for sterling

By Validus | 14 May 2026 | 5 min read

Marc Cogliatti, Head of Market Risk Strategies

Key takeaways:

- Expectations that the Labour party would lose close to 1,500 seats in last week’s local elections led to an initially muted response from markets. This changed on Monday as calls for the Prime Minister to step down intensified, yet he remains adamant that he will not resign

- There are concerns that a change of leadership could result in a relaxation of fiscal rules and increased spending and spark a market reaction similar to the one that resulted in Liz Truss’ demise

- Sterling sits within sight of its highest level against the dollar in more than 3 years. For those concerned about higher GBP borrowing costs, now feels like a sensible time to be reviewing risk profiles and reassessing whether any action needs to be taken

"Unless the government delivers urgent and significant change, it's clear the Prime Minister cannot lead us into the next election." Louise Haigh (former cabinet minister)

We all knew that last week’s local elections in the UK were going to be bad for Labour. Markets were not questioning whether they would have an impact. Instead, the main question on our minds was, ‘how bad will it be?’

Markets were expecting Labour to lose ~1,500 seats and for once, they were right – the actual number of lost seats totaled 1,498. That goes a long way to explaining why we initially saw relatively little reaction in the markets. If anything, sterling began the week a touch stronger and Gilt yields were down slightly as some of the UK risk prima was priced out. That flipped late in Monday’s session as calls for the Prime Minister to step down intensified, but for now at least, Sir Keir Starmer is adamant that he is not going anywhere.

The question now, is for how long? If no challenge comes from a more high-profile candidate in the next day or so, momentum to oust the Prime Minister may fizzle out, but it feels like it is only a matter of time until the question is raised again.

Why does this matter for markets?

There remains uncertainty around who would replace Sir Keir Starmer in the event of his resignation. Former deputy Prime Minister, Angela Rayner, and Mayor of Greater Manchester, Andy Burnham, are seen as leading candidates and both lean to the left of the current Prime Minister politically. The concern for markets is, therefore, that a change of leadership would likely result in a relaxation of Rachel Reeves’ fiscal rules and increased spending. This, in turn, brings back memories of the policies and market reaction that resulted in Liz Truss’ demise.

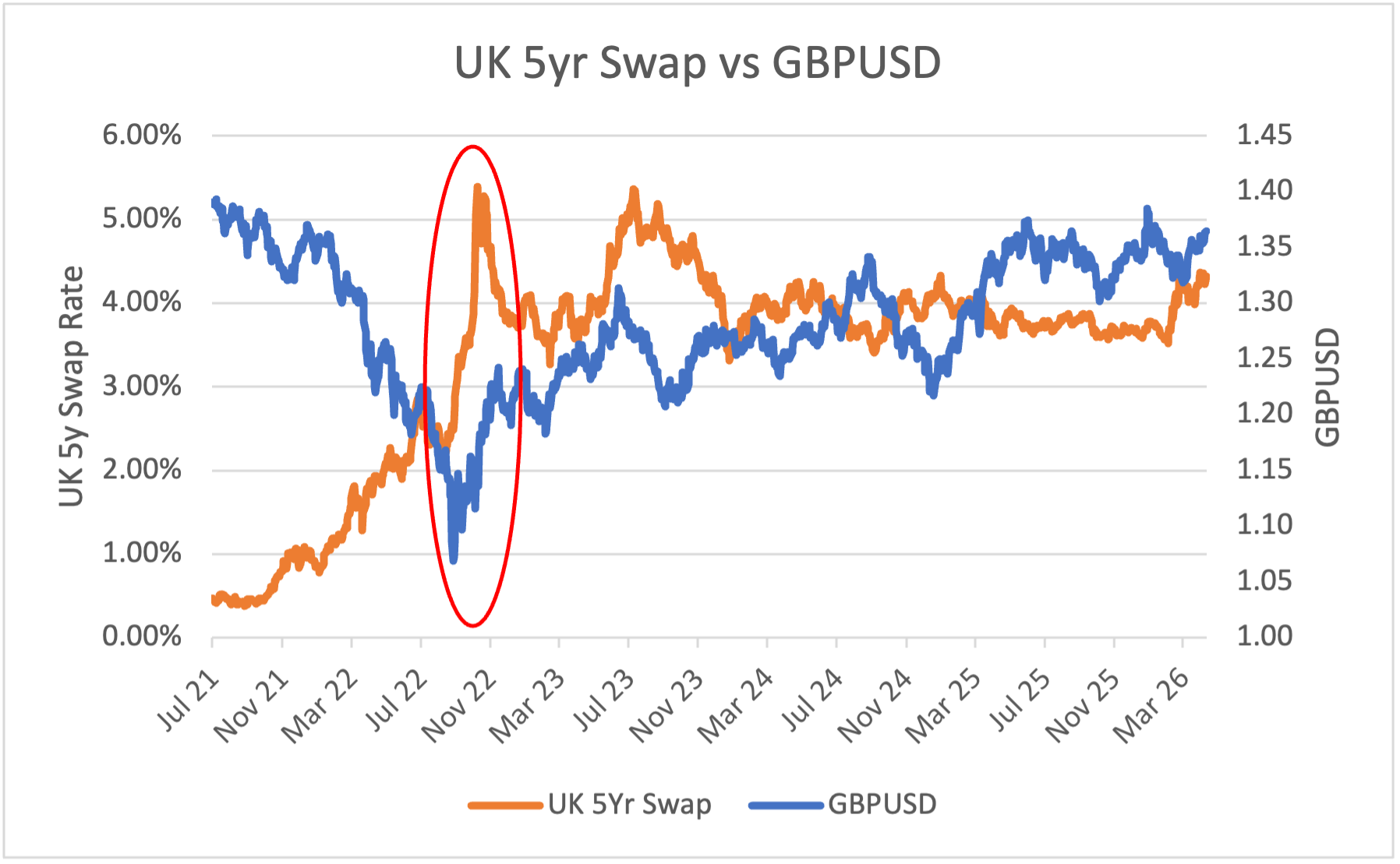

Chart 1: UK 5yr Swap vs GBPUSD

Source: Validus/Bloomberg

How should clients be thinking about this risk?

While there is no one-size-fits-all approach across our client base, for clients concerned about higher GBP borrowing costs, now feels like a sensible time to be reviewing their risk profile and reassessing whether any action needs to be taken.

Clearly, the challenge is that rates are elevated by recent standards (the 5-year swap rate currently sits at 4.35% and has ranged between 3.3% and 4.4% over the past 2.5 years) and a far cry from what we became used to prior to 2022. Meanwhile, volatility has shot up, meaning that interest rate caps are also more expensive. That said, the risk that rates continue to rise another 100+ bps from here is not beyond the realms of possibility.

Meanwhile in FX, sterling sits within sight of its highest level against the dollar in more than 3 years, which is mainly due to a weaker USD across the board. While interest rate differentials continue to add a cost to hedging, this still feels like attractive levels for USD vehicles to be taking GBP risk off the table.

Our Risk Advisory and Capital Markets teams remain on hand to discuss individual cases and suggest appropriate risk management strategies.