Rapid Read Report

12 March 2026RISK INSIGHTS

Oil, inflation and escalation: macro points to ponder

By Validus | 19 March 2026 | 5 min read

Harry Woolman, Global Capital Markets Associate

The 2020s have delivered no shortage of upheaval – the Covid pandemic, Russia’s invasion of Ukraine and the corresponding spike in inflation, and “Liberation Day” tariffs, among other market moving shocks. Now, adding to the list is the US-Israeli war with Iran, presenting another major headwind for economies and policymakers alike. In our note last week [Dollar dominates as risk appetite dissipates], we highlighted the dollar’s immediate appeal, supported both by the US economy’s status as a net oil exporter and the dollars haven role as the world’s reserve currency. This week, we examine the ramifications of the conflict in greater depth, looking at how investors and consumers may already be starting to feel the strain as the war enters its third week

Key takeaways:

- The war in Iran has triggered a sharp oil shock, with Brent surging and short-term energy volatility spiking in a way that recalls February 2022

- The fallout is already reaching consumers, with higher gasoline, diesel, and European gas prices pointing to a renewed inflationary impulse

- Markets have responded by repricing central bank expectations, as higher inflation risks and rising swap and breakeven rates complicate the outlook for policymakers

- Emerging markets and global supply chains look especially exposed, reinforcing the need for dynamic strategy and protection against unhedged risk

How the shock is spreading

As with February 2022, the near-term energy market shocks have been profound. With the Strait of Hormuz effectively shut, Brent, the global oil benchmark, has whipsawed from $79/barrel to just under $120, and was sitting at $103 at the time of writing. Unsurprisingly, these moves have triggered a corresponding spike in near-term volatility, with Brent one-month implied volatility rising by more than 120% since the end of February.

Chart 1: Brent Oil – One-month implied volatility. Ukraine and Iran price shocks compared in the two circles.

Source: Bloomberg, as of 17th March 2026

Last week saw a host of central bank commentary in Europe, with the European Central Bank’s (ECB) Peter Kazimir making a particularly salient point: markets can call upon lessons from February 2022 as they seek to second guess just how far this shock will spread. Intuitively, this notion, along with the sheer volume of oil supply affected across the Middle East, goes a long way to explaining both the speed and magnitude of the price moves over the past two to three weeks.

Transmission to the consumer is already being felt. Gasoline and diesel prices have climbed c. 49% and 27% respectively for US consumers. In Europe, the picture is even bleaker: a 65% price increase for one-month TTF natural gas since the end of February, at a time when governments race to stockpile ahead of the winter, leaving demand particularly inelastic to elevated prices.

Furthermore, a broader look at global supply chains flashes additional warning signs. Qatar, having already suspended operations at the world’s largest LNG export hub, is also a critical supplier of helium. This inert gas is a fundamental component to semiconductor manufacturing, so at a time of surging demand for advanced chips, any prolonged disruption poses medium- to longer-term concerns.

Inflation: Expectation vs. Reality

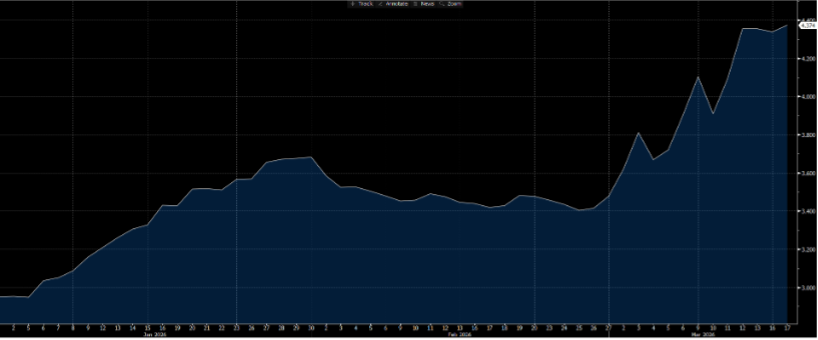

Predictably, that pass through is now showing up in higher inflation expectations, with risks skewed to the upside. The UK consumer, already weighed down by a prolonged period of elevated price pressures, anemic economic growth and political uncertainty, is seemingly gearing up for another leg higher in inflation. Breakeven rates – a measure of expected inflation over a given timeframe – have spiked 25% (90bps) over the past two and a half weeks.

Chart 2: UK 2-year Breakeven Rate

Source: Bloomberg, as of 17th March 2026

Ahead of a critical week of central banks – with the ECB and Bank of England due to announce policy decisions on 19 March - monetary policymakers are largely beholden to the whims of oil markets, as they were in February 2022. Markets briefly went so far as to price in two 25bp ECB hikes by year-end, though that has since been pared back to around one and a half hikes at the time of writing.

Should inflation – both realized and expected – continue to climb in the near-term, we’ll likely see rates markets ratchet higher as investors position for more aggressive central bank action. UK swap rates have also risen by more than 50bp since the conflict began, demonstrating just how fragile risk appetite remains.

Emerging markets under pressure

In keeping with the broader flight to safety, EM assets have come under greater pressure than their developed market counterparts. Measures adopted in some jurisdictions – including temporary school closures in Pakistan, and work-from-home directives for government employees in Thailand and Vietnam – highlight just how far-reaching the implications of the conflict could become, as governments seek to limit oil consumption.

Additionally, with the shifting strategic ambitions of the US, Kharg Island has emerged as a focal point for recent military activity. The island accounts for 90% of Iran’s crude exports - roughly 1.1 to 1.5 million barrels a day, according to Reuters – and now appears to be central to escalation risks. China, the largest buyer of Iranian crude, has a vested interest in the continued operation of those facilities. If the island’s oil infrastructure were to be struck, as its military assets already have been, and China were drawn deeper into the conflict, it is hard to see any real winners, especially given the likely corresponding spike in energy prices.

Investors should be wary of unhedged exposure, and strategy must remain dynamic as the conflict continues to evolve. Mitigating exogenous shocks and building resilience to key return metrics remains sacrosanct, and the right adviser can certainly play an important role in that process.