The “One Big Beautiful Bill” twist

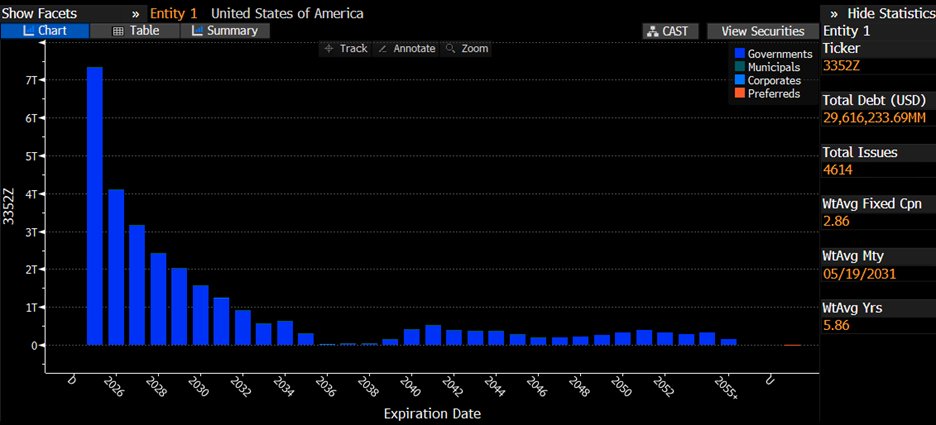

The “One Big Beautiful Bill” adds a new dimension to this already heavy maturity wall. It allows – and the budget effectively requires – USD 2 trillion to 4 trillion of extra issuance by the end of 2025.

Secretary Bessent’s recent remarks, including last week’s Bloomberg TV interview, outline how the Treasury intends to tackle this: focus on short-term securities, especially T-bills, thereby shortening portfolio duration. With long rates at current levels, this is logical. Interest on the national debt already approaches USD 800 billion this year; locking in today’s long yields while confronting the maturity wall could add as much as USD 2 trillion in debt servicing costs.

It’s no surprise, then, that the President Trump is pressing for lower rates by continuing his persistent attacks on Chair Powell.

A short-term shield – with caveats

By issuing T-bills and rolling them, the Treasury hopes to weather the high-rate cycle and lengthen duration only once the Fed begins cutting. In essence, the Treasury will sell very short-dated debt while buying back – or simply letting lapse – longer bonds. The approach is rational and should avoid near-term disruption, yet it carries risks:

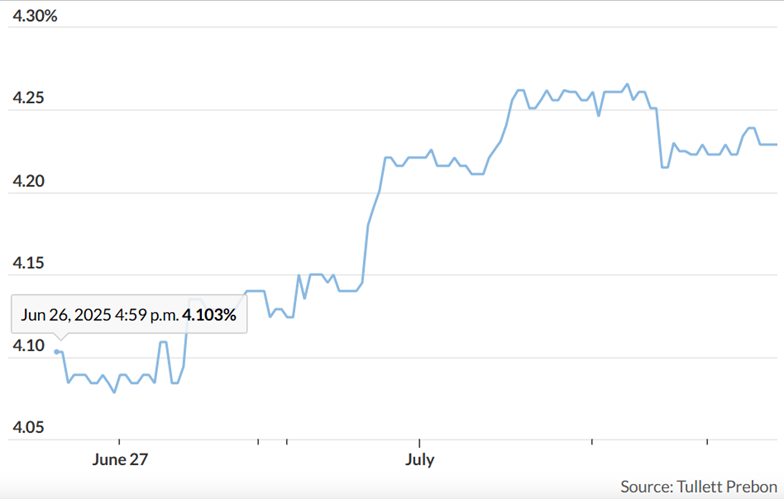

- Short-end pressure: one-month T-bill yields have risen over the past fortnight as supply has grown. With more bonds maturing and new BBB-related issuance ahead, the depth of investor appetite merits close watch.

- Long-end scarcity: a sustained drop in long-bond issuance could tighten liquidity and limit availability for investors that rely on these instruments, such as insurers and pension funds.