US Fed’s 2025 tightrope: balancing data, mandate and political heat

2 July 2025

Trump turns up the tariff temperature

16 July 2025INSIGHTS • 9 July 2025

The Treasury’s Yield Curve Play: the 2025 Maturity Wall

Kambiz Kazemi, Chief Investment Officer

“Why would we do it (terming out US debt issuance)? We are more than one standard deviation above the long-term rates. They time to do that would have been in 2021, 2022.”

Secretary Scott Bessant, 30 June 2025

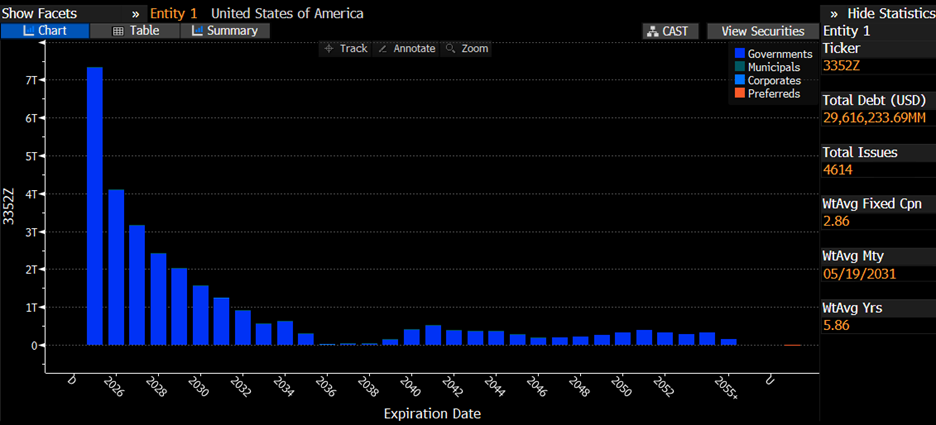

A wall of maturities

2025 is the historic “maturity wall” for the US treasury: almost USD 9.2 trillion of outstanding debt was falling due this year - roughly a quarter of the entire national debt.

The Treasury has several levers at its disposal to ensure the smooth functioning of the market despite such a lumpy expiry schedule. Notably, by laddering new supply and adding liquidity back-stops such as regular buy-backs of off-the-run bonds.

Chart 1: US debt maturing per fiscal year (trillion USD)

The “One Big Beautiful Bill” twist

The “One Big Beautiful Bill” adds a new dimension to this already heavy maturity wall. It allows - and the budget effectively requires - USD 2 trillion to 4 trillion of extra issuance by the end of 2025.

Secretary Bessent’s recent remarks, including last week’s Bloomberg TV interview, outline how the Treasury intends to tackle this: focus on short-term securities, especially T-bills, thereby shortening portfolio duration. With long rates at current levels, this is logical. Interest on the national debt already approaches USD 800 billion this year; locking in today’s long yields while confronting the maturity wall could add as much as USD 2 trillion in debt servicing costs.

It’s no surprise, then, that the President Trump is pressing for lower rates by continuing his persistent attacks on Chair Powell.

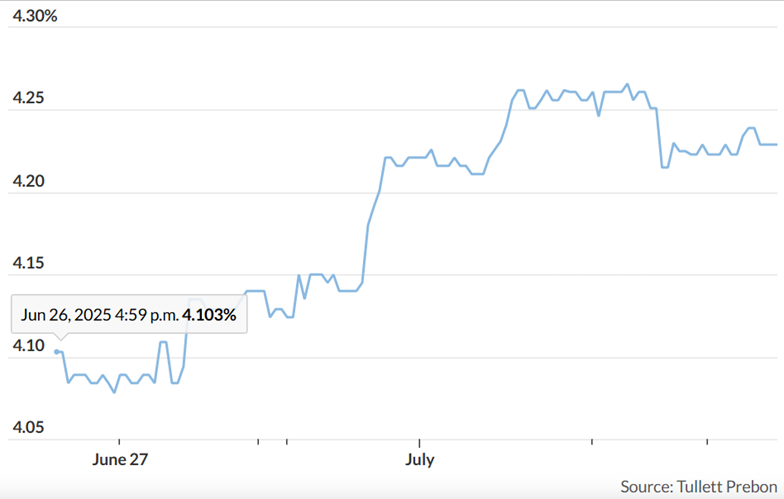

A short-term shield – with caveats

By issuing T-bills and rolling them, the Treasury hopes to weather the high-rate cycle and lengthen duration only once the Fed begins cutting. In essence, the Treasury will sell very short-dated debt while buying back - or simply letting lapse - longer bonds. The approach is rational and should avoid near-term disruption, yet it carries risks:

- Short-end pressure: one-month T-bill yields have risen over the past fortnight as supply has grown. With more bonds maturing and new BBB-related issuance ahead, the depth of investor appetite merits close watch.

- Long-end scarcity: a sustained drop in long-bond issuance could tighten liquidity and limit availability for investors that rely on these instruments, such as insurers and pension funds.

Chart 1: Yield on 1-month Treasury Bill

Beware of Assumptions

It’s important to note the entire plan rests on the assumption that the Fed will oblige with rate cuts. Markets currently price in two reductions by year-end, and Chair Powell’s term ends on 15 March 2026, yet two awkward outcomes could throw the strategy off course. First, if inflation proves stubborn and delays those cuts, the Treasury could find itself trapped in an ultra-short stance for longer than intended. Second, the Fed might deliver the cuts, but long yields could remain high - or even rise - if term premia widen amid fresh concerns over the government’s credit profile after the debt-ceiling lift. With less long-dated supply in the market, that part of the curve could become increasingly sensitive to the moves of a handful of large players, inviting bouts of volatility reminiscent of the UK gilt episode, and become prone to “accidents” along the way.

Going forward, duration risk will be front and centre - and, if investors begin reducing their exposure to duration, that caution can prove self-fulfilling. Caveat emptor.

Be the first to know

Subscribe to our newsletter to receive exclusive Validus Insights and industry updates.