Real Return Bonds (RRBs) have long been the go-to tool for inflation protection, offering interest and capital payments indexed to the Consumer Price Index (CPI), though often at the cost of low real yields. Today, their usefulness is somewhat curtailed due to:

- a shrinking and illiquid market

- limited supply on the secondary market as holders rarely sell

- their lower yield given they offer no credit premium; and

- the federal government halting new issuances of RRBs in 2022.

Alternatives to Real Return Bonds

With the limitations of RRBs, investors have increasingly turned to alternative strategies to manage inflation risk while seeking more attractive returns. Over the past decade, many pension plans have diversified into alternative investments such as real estate, infrastructure, commodities, and private equities with inflation-sensitive characteristics. Some have even looked beyond Canadian borders, incorporating U.S. Treasury Inflation Protected Securities (TIPS) into their portfolios.

However, not all of these alternatives offer a robust inflation protection. Real assets can be subject to liquidity constraints, accessibility issues, and market volatility, which may limit their effectiveness depending on the economic environment. TIPS, while structurally similar to RRBs, are tied to the U.S. Consumer Price Index. Although the U.S. and Canadian CPIs have shown about 80% correlation since 1982, annual variations can differ by up to ±3%, and the U.S. CPI has generally grown faster, potentially reducing the precision of inflation hedging for Canadian investors.

An Innovative Take on Inflation Resilience

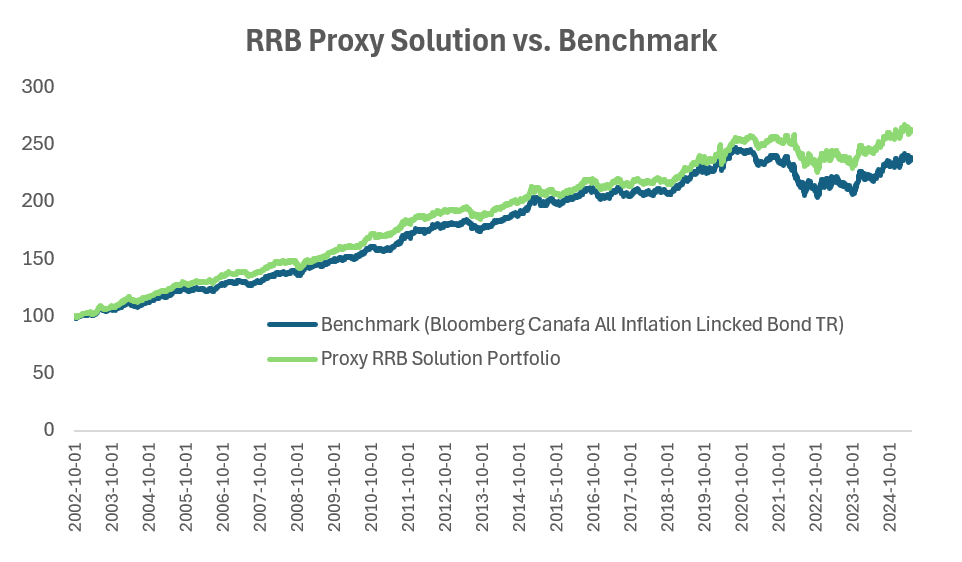

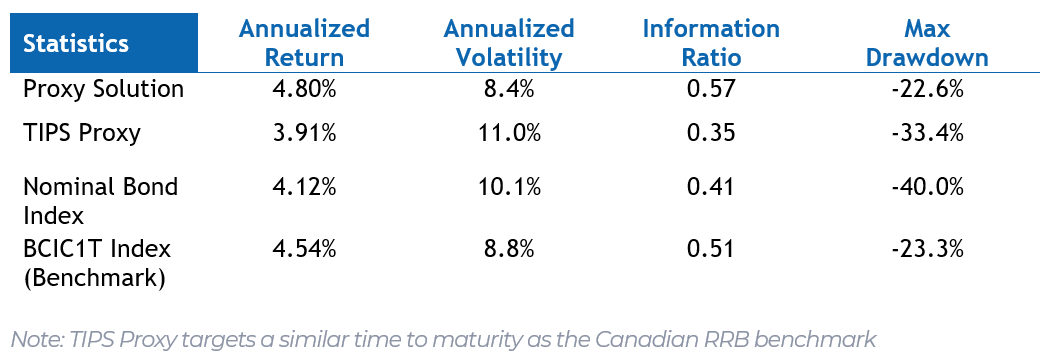

Since the federal government ceased issuing Real Return Bonds in 2022, there has been widespread discussions about finding effective substitutes for inflation protection. Ideally, these solutions should work in tandem to manage both inflation and interest rate (duration) risks.

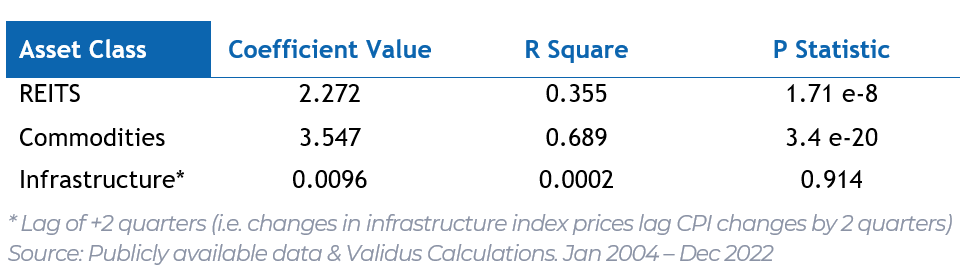

To evaluate the relative attractiveness of these inflation protection substitutes, we looked at their excess returns relative to the excess returns of TIPS versus nominal bonds, a proxy for breakeven rates. We used TIPS because of the availability of the data and liquidity of U.S. alternative assets and indices. The conclusion holds for the Canadian environment. The results, summarized in Table 1, highlight the potential of selected alternative asset indices, to deliver inflation protection based on the regression of their excess return versus that of TIPS. A higher R-squared coefficient indicates a stronger relationship between the alternative asset and the TIPS.