“A Blairite, a Brownite, a Milibandite and a Corbynite walk into a pub and the barman says, ‘Hello, Mr. Burnham.’” – well-known quip associated with Andy Burnham.

Our note last week highlighted what many had anticipated – massive losses for the Labour Party at the recent local elections. Since then, UK assets have once again been thrown into turmoil, heaping pressure on Prime Minister Sir Keir Starmer and exacerbating the sense of tumult in Westminster.

Long considered a relative bulwark of political stability, the UK is now staring down the barrel of a sixth Prime Minister in 10 years.

From stability mandate to political fragility

When Labour swept to power in July 2024 with a decisive election victory, many had hoped the substantial majority secured by Starmer’s government would usher in a period of political stability.

However, persistent cost-of-living pressures and anaemic economic growth have seen support for the incumbent government slide since it set foot in Downing Street. Simultaneously, the rise of the political periphery – namely Reform UK under Nigel Farage and the Green Party under Zack Polanski – highlighted growing voter discontent, which was emphatically voiced at the recent local elections.

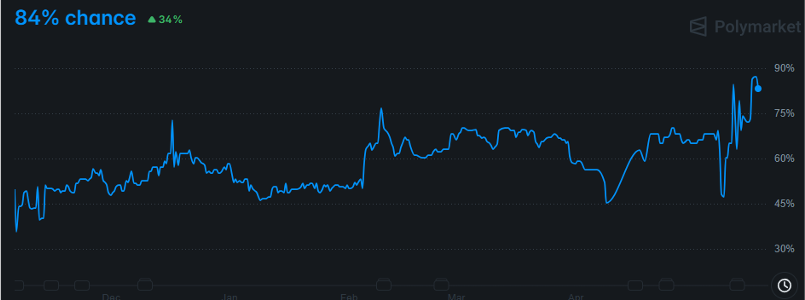

Labour’s poor performance culminated in four cabinet-level resignations late last week, with former Health Secretary Wes Streeting emerging as the highest-profile dissenter as he prepares to challenge Starmer.

However, these departures were arguably overshadowed by the resignation of Labour backbencher Josh Simons, MP for Makerfield. His departure opened the door for Andy Burnham to contest the seat, potentially giving him a route back into Parliament and, by extension, a pathway to Downing Street.

A looser fiscal turn?

Burnham’s omnipresence in Labour politics over the last 20 years – captured by the joke in this article’s sub-heading – has included two failed leadership bids, alongside a well-regarded tenure as Mayor of Greater Manchester.

His comments last year suggesting the UK has “got to get beyond this thing of being in hock to the bond market” have unnerved investors considering the prospect of his national leadership. Nonetheless, the political hurdle to greater fiscal largesse now appears materially lower after the local elections than under the incumbent Starmer-Reeves administration.

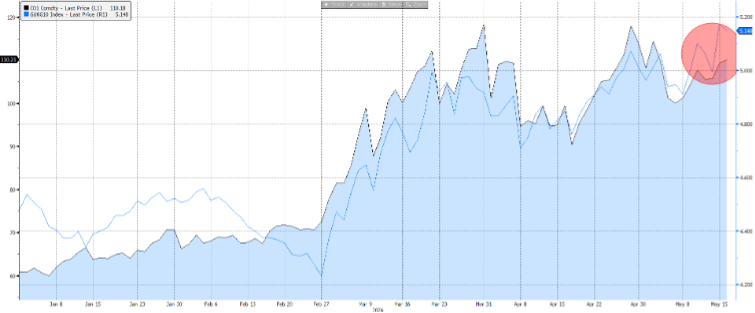

More recently, Burnham floated the idea of an additional £40 billion in borrowing, with supplementary defence spending also falling outside the scope of any fiscal rules. Coupled with the global bond rout that has unfolded since the Middle East conflict began, this has weighed heavily on long-dated UK gilts.

Last week saw 30-year yields jump 21 basis points to their highest levels this millennium, while 10-year yields also reached post-2008 highs. Indeed, 10-year rates rose by more than 10 basis points last Friday, highlighting the extent to which UK political developments are contributing to longer-term borrowing costs, beyond the impact of geopolitical conflict alone.

For investors, therefore, the concern is not merely political instability. It is the prospect that a post-Starmer Labour leadership could usher in a materially looser fiscal stance.