Like any relationship, though, this ‘correlation’ is far from perfect, and its strength constantly fluctuates. After a period of relative stability, we suddenly find ourselves at a point where the correlation appears to have broken, prompting us to question whether what we’re seeing is just a temporary shift–or the start of something more permanent.

A few points for consideration:

- Correlation hiccups

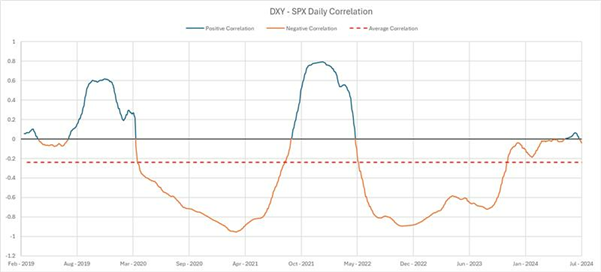

Over the past five years, there were two periods – H2 2019 and Q4 ’21 – Q3 ’22 – when the DXY and SPX had a positive correlation before reverting. What’s to say that the next 3-6 months won’t follow the same pattern? Experience suggests not getting too distracted by short term volatility. It’s also worth noting that while U.S. stocks (especially tech stocks) have been under heavy selling pressure, European indices have done relatively well over the past couple of months, suggesting a reduction of an overweight position in US equities rather than a broader ‘risk off’ move.

- The tariff angle–a reversal in sight?

Much of the recent market volatility has coincided with uncertainty surrounding Trump’s tariff policies. Whilst it might be presumptuous to think he’s simply calling everyone’s bluff and will revert to a more pragmatic stance, it’s not beyond the realms of possibility that he could abolish the tariffs that have been put in place, prompting a reversal in recent market moves.

- Yield differentials take centre stage

Between the Global Financial Crisis (GFC) and COVID, when global interest rates hovered near zero, risk sentiment was the primary driver in currency markets. As interest rate volatility has picked up, yield differentials have once again become the primary focus on a day-to-day basis and there’s no reason to think this won’t continue.

- De-dollarisation—momentum or mirage?

In recent years, there’s been plenty of big-picture talk around ‘de-dollarisation’ and the search for an alternative to the dollar as the world’s global reserve currency. Whilst this is not a process that happens overnight, momentum may be starting to build.

- The enduring appeal of U.S. Treasuries

The absence of an obvious alternative to U.S. Treasuries as a safe haven means there will continue to be demand for US bonds, even if its not quite as strong as it has been historically.