Action at the All England Lawn Tennis Club is firmly underway, yet for investors in UK assets, another Andy Murray is attracting attention. Following Keir Starmer’s resignation as Labour leader – and therefore Prime Minister – on June 22, Andy Murray Burnham (yes, that really is his middle name) has emerged as the overwhelming favorite to become Britain’s fifth Prime Minister since 2020.

The defining question for investors, therefore, is not whether Andy Burnham becomes Prime Minister, but whether any government can escape the increasingly narrow fiscal constraints imposed by weak growth, elevated borrowing costs, and rising structural spending pressures.

Labour’s formal nomination process for leadership candidates begins on July 9 and runs until 6 p.m. on July 15. As a reminder, only those with backing from at least 20% of sitting Labour MPs (81 out of 403) will battle it out to lead the party. Current standings suggest Hawkeye will not be required to determine the remaining candidates, as Labour heavyweights Wes Streeting and Darren Jones have endorsed Makerfield’s newest MP to lead the party into the next general election, due in 2029.

Inheriting a Fraught Fiscal Policy

Events last weekend typified how exposed the UK’s fiscal outlook remains to external shocks, with renewed strikes between the US and Iran triggering a brief bout of market volatility, as the conflict continues to present upside risks to global inflationary pressures. The renewed focus on fiscal resilience comes as one of Keir Starmer’s final acts in office was to announce a new defense funding package.

Totaling £15 billion in additional spending commitments, the package leaves the incoming government needing to identify a further £4.7 billion of funding in its next Budget. Absent meaningful economic growth, Burnham will face the likely unenviable task of choosing between increased taxation and/or austerity measures. Put another way, every pound of “new” spending increasingly crowds out investment elsewhere.

Additionally, as long as uncertainty over US-Iran negotiations remains, inflationary pressures will stay elevated. Higher inflation expectations are likely to keep rates elevated, ensuring debt-servicing costs remain structurally higher than they were before the pandemic. This was made clear by May’s fiscal deficit data, which soared to £23.9 billion – a 30% jump year over year and £5.6 billion above estimates. It therefore stands to reason that whoever Burnham chooses to succeed Rachel Reeves (if anyone at all) will be the next test for bond markets, ahead of the autumn Budget in three to four months’ time, with debt affordability continuing to pose a problem that any future Chancellor has limited scope to alleviate in the current environment.

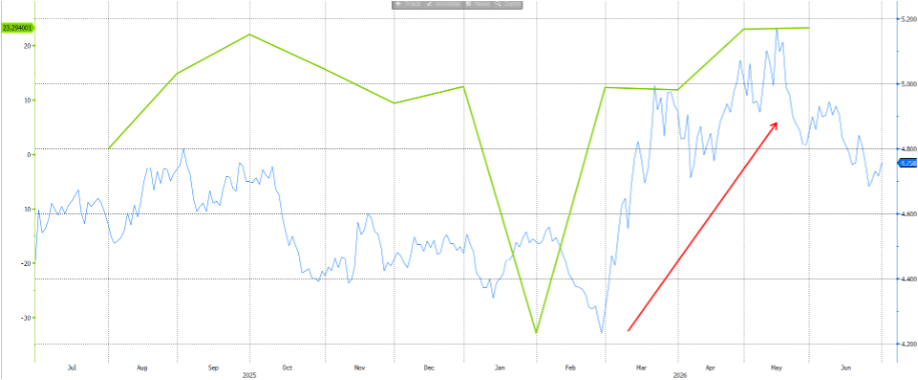

The challenge of higher borrowing costs has been exacerbated by Reeves’ self-imposed fiscal rules, which Burnham has pledged to adhere to. Should borrowing increase, or unfunded spending plans come to fruition, expect government interest payments to rise and the fiscal outlook to deteriorate further. The negative feedback loop between the government’s fiscal health and elevated gilt yields would then prove even tougher to break. Any perception that borrowing will rise faster than planned risks a renewed increase in gilt yields, further tightening the fiscal constraints facing the next government, as evidenced by the chart below.

Chart 1: UK fiscal deficit (green line) vs. 10-Year gilt yield (blue line)