Solid jobs, sticky prices – the Fed’s high-wire act

The macro picture looks resilient, yet the path ahead is clouded by trade uncertainty.

The labour market – central to the Fed’s mandate – remains firm: the unemployment rate has hovered near 4 per cent for a year, and non-farm payrolls have averaged about 150,000 a month in 2025, a slowdown from 2024 but far from recessionary. Wage growth still outpaces inflation, though it has moderated, hinting that supply and demand for labour are still broadly in balance.

Inflation, however, is proving stickier. The downtrend of 2023-24 has stalled, with headline PCE running at 2.3 per cent and core PCE at roughly 2.7 per cent – both above the Fed’s 2 per cent goal. Short-term inflation expectations have edged higher, largely on the prospect of fresh tariffs that would raise costs for businesses and consumers alike.

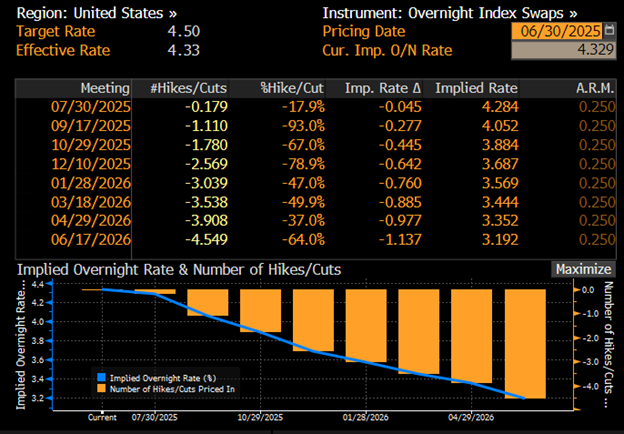

Against this backdrop the Fed has kept the funds-rate target at 4.25-4.50 per cent since December 2024, following three cuts earlier that year. Powell frames the stance as a “wait-and-see” pause: policymakers want clearer evidence of how the new tariff regime will play out before acting again. They are acutely aware that tariff-driven price rises could rekindle inflation even as growth cools, reviving the unwelcome spectre of stagflation.