Only six months ago, the notion that investors might seek alternatives to the dollar’s safe haven and reserve currency status seemed remote (though, in hindsight, perhaps the warning signs were there). Today, this prospect seems much closer, even if it proves more challenging than it appears.

When the dollar first started to tumble back in January, following Trump’s inauguration, the euro struggled to gain traction. It was weighed down by assumptions that the Eurozone would be a primary target for tariffs, and that the European Central Bank (ECB) would need to adopt a more accommodative stance to shore up economic growth. Those assumptions turned out to be correct; however, since early February, the euro has been one of the G10’s best-performing currencies, outpaced only by the Swedish Krona and the Norwegian Krone.

A significant part of this move can be attributed to investors—particularly European investors—who had previously held large positions in US assets and are now rebalancing as American stocks and bonds lose some of their allure. How far this trend extends beyond hedge funds to more conservative, long-term investors such as pension funds, and ultimately central bank reserves, remains uncertain. Still, if market participants are indeed searching for viable alternatives to the dollar, the Eurozone stands out as the most credible option so far.

The question we find ourselves asking is whether the Eurozone economy can handle a strong euro.

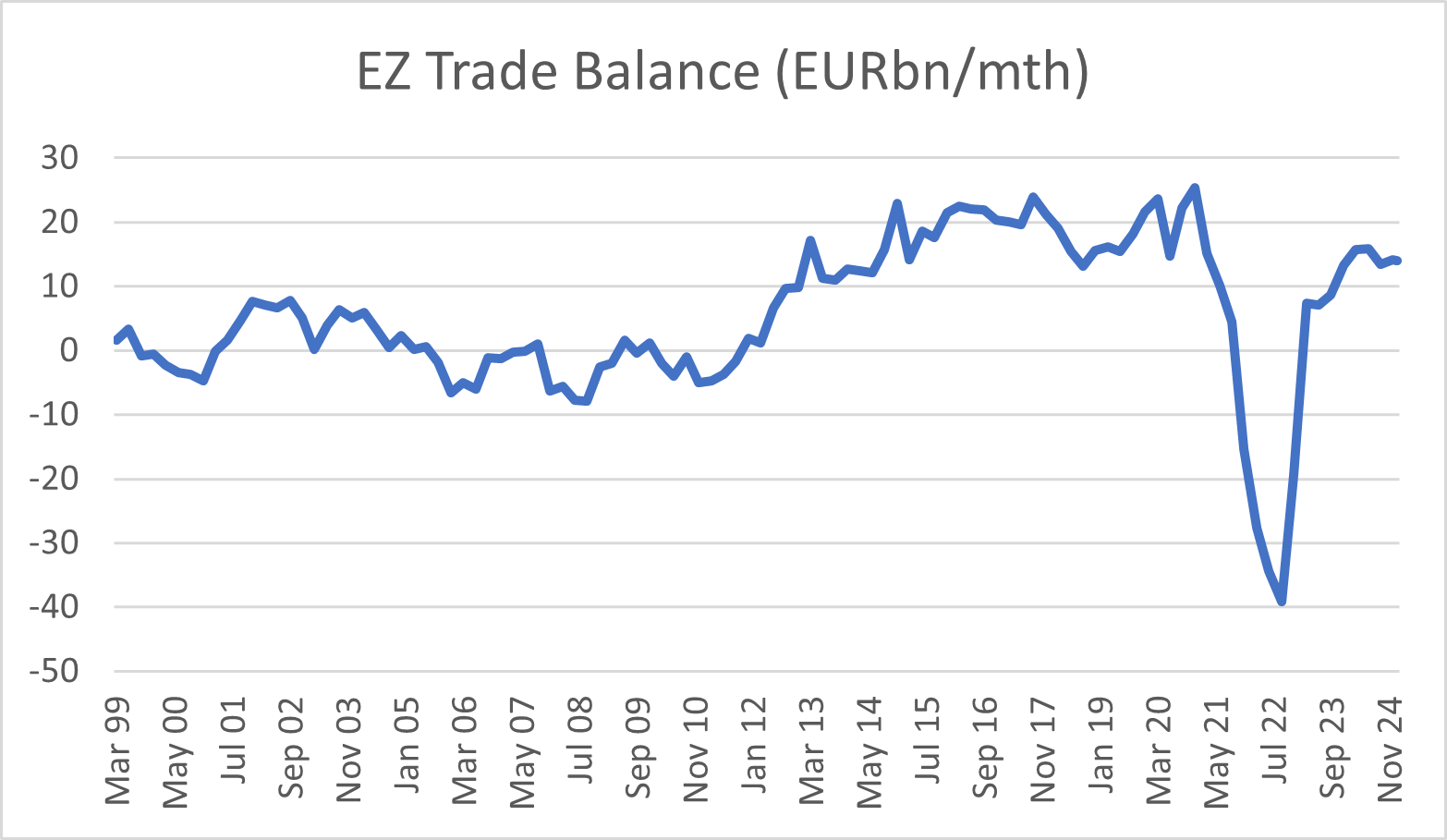

The Eurozone has long been a net exporter of goods to countries outside the European Union. Looking back over the past 25 years since the inception of the single currency, the average monthly trade balance has been ~€5.6bn. Narrowing this to the past 10 years, the surplus has more than doubled to approximately €11.3 billion per month, suggesting that trade has benefited from a relatively weak euro.

Focusing on the Eurozone’s trade with the United States, the monthly surplus stands at roughly €10 billion (much to the chagrin of Trump). Should he proceed with higher tariffs, that surplus is likely to fall, and a stronger euro would only add to the pressure. This, in turn, could weigh on growth and is fuelling fears of recession.