The outlook for US rates has shifted sharply in recent months.

Expectations that the Federal Reserve would deliver two to three quarter-basis point cuts have faded, as the conflict with Iran pushed oil prices up and revived concerns about global inflationary pressures.

The US administration continues to call for looser monetary policy, but markets are increasingly questioning whether the Fed has room to oblige. It remains to be seen how their select new Fed Chair Kevin Warsh will steer US policymakers.

Before last week’s jobs report, markets were already leaning towards a more hawkish path. Markets were pricing in a 63% probability of a 25bp Fed hike before year end, with a quarter point increase fully priced by the March 2027 meeting.

Those expectations hardened after Friday’s non-farm payrolls report showed the US economy added 172,000 jobs in May, comfortably above the consensus forecast of 88,000. The stronger-than-expected labour market print has strengthened the case for higher rates, particularly if inflationary pressures remain elevated.

Markets are now fully pricing in a 25bp hike by year-end, with a further increase expected late in the first quarter or early in the second quarter of 2027.

Dollar gains as risk sentiment weakens

Unsurprisingly, the prospect of higher rates has weighed heavily on risk sentiment, with the S&P 500 closing down 2.64% on Friday, while the dollar has advanced against its major peers, supported by the prospect of higher yields.

The key question is whether the latest data tilts the balance of risk back in favour of a stronger dollar or whether its simply more noise in a volatile market.

EURUSD breaks recent support

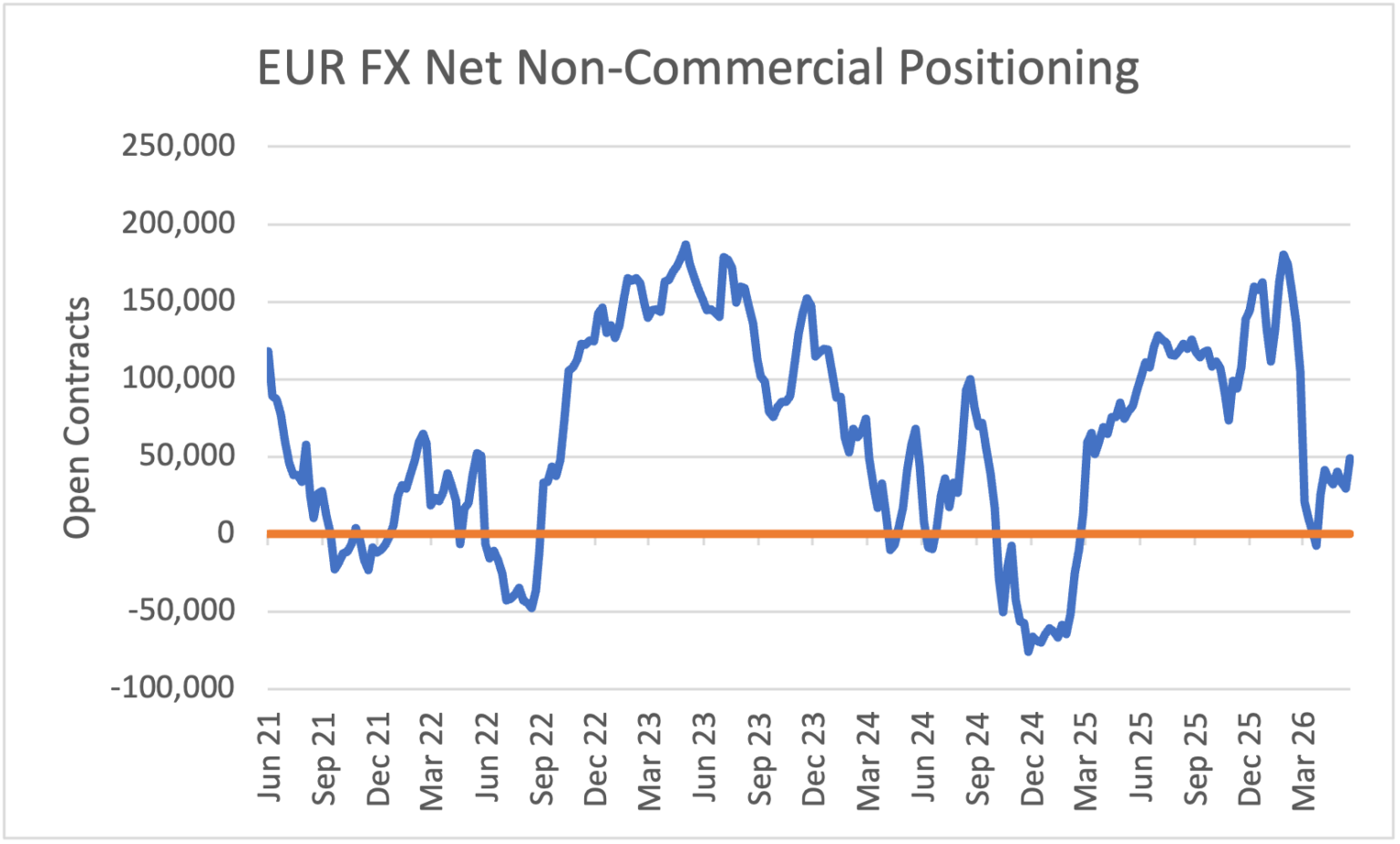

Futures positioning indicates speculative traders are net long EUR, but only modestly so (see chart below). That leaves plenty of scope for the dollar to extend recent gains if investors continue to price in a more hawkish Fed path.

From a technical perspective, EURUSD broke the 1.1575/80 support zone that has held in recent weeks. More meaningful support now sits around the 1.1400/50 region (Aug ’25 low and Mar’26 low). A break here would refocus attention on 1.1000 in the weeks / months ahead.